What is a factor?

A factor is a financial representative that provides businesses with a unique way to manage cash flow by purchasing their accounts receivable, typically at a discounted rate. This process is known as factoring and it allows companies to convert their outstanding invoices into immediate working capital without waiting for their customers to pay.

The factor assumes the responsibility of collecting payments directly from the customers associated with the invoices and charges a factoring fee for it. In addition to providing immediate cash flow, factors often offer additional services, such as managing credit checks on customers and providing detailed reporting. These services can save businesses time and resources, allowing them to focus more on their core operations.

This is why invoice factoring is a useful process for businesses. Here’s how the process unfolds.

Compare Invoice Financing Quotes Today

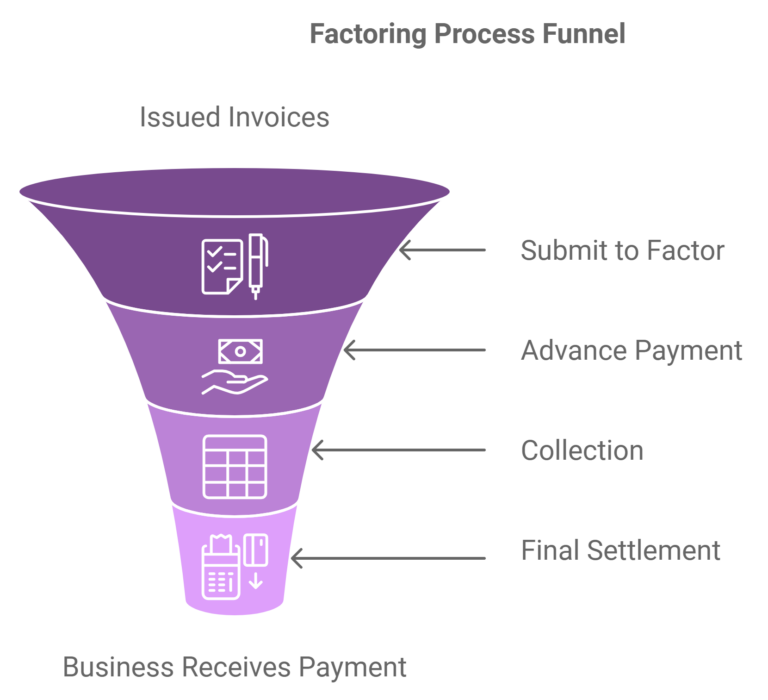

Process of factoring in business

Now that you’ve understood what is factoring in business, let’s look at its process.

- Invoice issuance: The business issues invoices to customers for goods or services provided.

- Submission to factor: It submits these invoices to a factor for review.

- Advance payment: Factor pays the business in advance, typically 70-90% of the invoice value.

- Collection: Factor takes over the responsibility of collecting payments directly from the customers.

- Final settlement: Once the customers pay, the factor deducts fees and the advance, then releases the remaining balance to the business.

What does a factor consider when factoring?

Since the factor is now responsible for handling customer payments, it’s only reasonable that it consider some points before making the decision whether to purchase the invoices from the business or not. Let’s look at what a typical factor sees.

- Creditworthiness of customers: The factor evaluates the credit history and reliability of the business’s customers, as they will be the ones paying for the invoices.

- Invoice value and volume: This is done to determine the potential risk involved in the factoring process.

- Payment terms: Longer payment terms might increase the risk for the factor, so they look at how long it typically takes for customers to pay.

- Outstanding debts: Existing debts or other financial obligations of businesses in the UK are considered to analyse overall risk.

Factoring example

This example of factoring will help you understand the process more clearly.

Yorkshire Apparel Ltd. secured a large order from a major retailer, High Street Fashion. The order is £100,000. Yorkshire Apparel Ltd. has to deliver the goods in 30 days, but the payment offered to High Street Fashion is 60 days from the date of delivery. To manage this cash flow gap, Yorkshire Apparel Ltd. opts for the factoring services of Bibby Financial Services on the following conditions:

- A factoring fee of 2% of the invoice value.

- Advance value of 85%.

Let’s look at the calculations:

Total invoice value = £100,000

Advance payment = £85,000

Factoring fee = £2000

Final payment to Yorkshire Apparel Ltd. = £13,000

According to a 2024 report by IBIS World, factoring companies’ revenue is expected to grow at a compound annual rate of 3.5% to £4 billion.

Benefits of a factor

Opting for a factor brings several advantages to your business.

Firstly, it helps businesses maintain a healthy cash flow. This allows the business to pay suppliers, employees and cover other operational costs without waiting for customers to settle their accounts.

Secondly, since factoring is not a loan, it doesn’t add to the business’s liabilities. The business sells its unpaid invoices and receives cash in return, which improves liquidity without increasing debt.

Thirdly, since factoring companies take on the responsibility of collecting the payments, this frees up the business’s resources and reduces the administrative burden, hence allowing it to focus on growth and other core activities.

Fourthly, the credit risk associated with invoices falls on the factor. This means if the customer fails to pay, the burden falls on the factor. This reduces the financial risk for the business and provides a layer of security.

Factor vs factoring company

In the world of finance, the terms ‘factor’ and ‘factoring company’ are often used interchangeably, but they do have some differences.

| Factor | Factoring company |

|---|---|

|

The ownership of the invoices is retained by the business. |

Operates on a broader scale, serving multiple industries and offering different services. |

|

Handles fewer clients and a limited volume of invoices. |

Had a wide client base. |

|

Maintains a more personalised relationship with the clients. |

Has a more formal and structured relationship. |

|

Collateral requirement |

Often requires significant collateral such as property.

|

Choosing the right factor for your business

When choosing the right factor for your business, it’s crucial to go beyond the surface-level considerations often discussed. Here are key points to consider in depth:

- Industry experience: Ensure that the factor has a deep understanding of your specific industry. Some factors specialise in certain sectors (like factoring for staffing companies) and can offer personalised solutions plus better rates.

- Flexibility in contract terms: Analyse the contract terms and look for the scope of flexibility in them. Some factors may lock you into long-term agreements or have rigid terms – this might not be suitable for your business’s changing needs.

- Transparency in fees: Beyond the factoring fee, examine all associated factoring fees, including those for additional services or penalties. Some factors may have hidden costs, so be wary of those.

- Customer service: Evaluate the level of customer support provided by the factor. Prompt and effective communication is essential, especially when dealing with financial transactions. Look for a dedicated account manager who is reachable on multiple communication channels like WhatsApp and email.

- Reputation: Research the factor’s reputation and financial stability (just like they do). A factor with a strong reputation is less likely to face liquidity issues that could impact your cash flow.

Choose the right factor for your business in the UK with ComparedBusiness

ComparedBusiness provides you with secure invoice factoring services from top factors in the UK. Just submit your requirements in less than 2 minutes and we will match you with them. You can choose the best option depending on your business needs.