At many points in the financial year, a business may need extra cash flow to manage its operations effectively or cover any unexpected expenses. This need could also arise during a slow business season, plans to scale business operations, or just a day-to-day lack of cash flow.

Whatever the reason may be, it all boils down to a shortage of cash liquidity in the business. To solve this problem, businesses choose financing solutions like a line of credit or a merchant cash advance.

This brings up an important concern of choosing the right financing solution for your business. Both options work differently and tend to suit different business industries. Let us learn about the differences between a line of credit and a merchant cash advance in this blog and see how they benefit businesses.

What is a line of credit?

A line of credit (also called a business line of credit or merchant line of credit) is a financing solution that acts like a safety net for businesses. Its working can easily be understood by comparing it to a credit card. With a line of credit, a business gets access to a set credit limit that it can use just like a pay-as-you-go plan and make repayments with an interest rate.

Next, we will discuss the multi-step process it goes through to apply and get approved for a line of credit financing solution.

How does a line of credit work?

Here is how businesses can access and use funds via a line of credit in 5 simple steps:

- A business recognises its need to maintain a backup fund to cover any unexpected expenses, get through a low sales period, or simply improve cash circulation in the business affected by delayed payments and a lack of working capital.

- The business then applies for a line of credit with a financial institution.

- Once the request gets approved, the business gets access to a maximum amount of credit that it can withdraw and use for business purposes.

- Funds are used when needed, and interest is only charged on the amount used, not the maximum limit.

- The set limit of a line of credit is recharged as the business pays the interest repayments. There’s no pressure to use the entire amount at once, and no interest is charged on unused funds by the business.

What is merchant cash advance?

A merchant cash advance (or merchant funding) is a financing option that allows businesses to obtain secure cash funding in exchange for a percentage of their future sales. Repayments are made from a portion of daily or weekly card sales (credit and debit) only. It is different from a traditional business loan because MCA doesn’t involve interest rates. Instead, the total repayment amount is calculated via a factor rate.

In the next sections, we will explain the concept of factor rate, how the process of MCA works, the business industries to benefit the most from MCA, and more.

How does MCA work?

The process of application and approval for MCA can be explained for businesses in 4 simple steps:

- The business applies for MCA funding by filling out an application form and providing basic details like past sales records and general business information to the provider.

The application gets reviewed and approved by the provider. - Depending on the provider, a business can generally access the funds within 24 hours to 3 business days.

- As soon as the business starts making sales, a fixed percentage (decided in advance) of its daily or weekly card sales is transferred to the provider. The repayment amount also changes based on sales volume. High sales mean quick repayments and vice versa.

- As soon as the business starts making sales, a fixed percentage (decided in advance) of its daily or weekly card sales is transferred to the provider. The repayment amount also changes based on sales volume. High sales mean quick repayments and vice versa.

Do you need a Merchant Cash Advance?

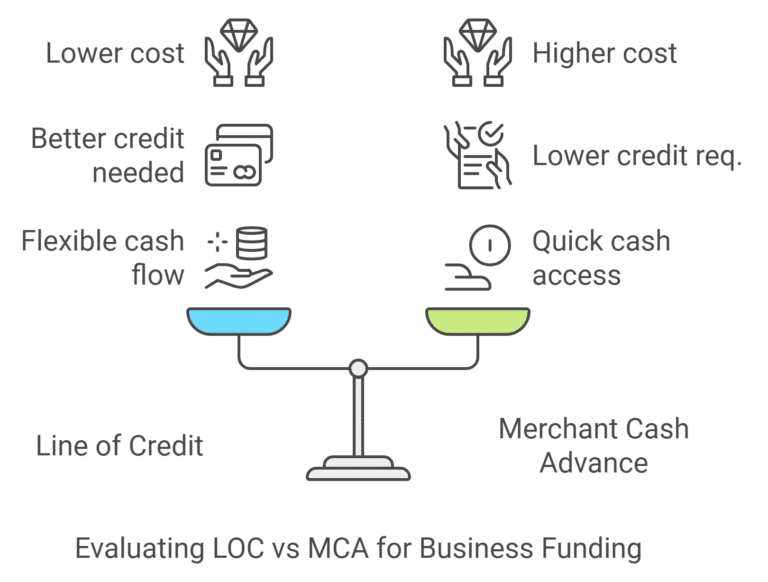

Line of credit vs Merchant cash advance: 5 differences explained

| Feature | Line of credit | Merchant Cash Advance |

|---|---|---|

|

Repayment schedule |

Flexible; you only pay interest on what you borrow, with control over when to repay. |

Automatic deductions from daily sales, based on a percentage. |

|

Eligibility and approval |

Requires strong credit, financial statements, and possibly collateral. |

Easier approval, even with bad credit, based on sales history. |

|

Cost of borrowing |

Generally lower interest rates, making it more affordable long-term. |

Higher cost due to factor rates (1.2-1.5), leading to greater overall expense. |

|

Funding speed |

Approval can take longer depending on credit; slower access to funds. |

Fast approval (24-72 hours); ideal for quick access to cash. |

|

Flexibility |

Revolving credit; can borrow again after repayment without reapplying. |

Lump sum with no flexibility for additional borrowing until a new agreement. |

1. Repayment schedule

With a line of credit, you have relatively more control over how you repay. The interest is charged on the amount of money used from the total amount borrowed. As long as you stick to the minimum payments, you are the one making decisions about when and how to repay.

On the other hand, an MCA automatically deducts a percentage of your daily or weekly sales according to the terms of your contract with your MCA provider.

2. Eligibility and approval process

A key difference between a line of credit and an MCA is the approval process. Lines of credit require strong credit scores, bank statements, collateral, and a long time for evaluating the application to decide if your business is eligible.

However, there are multiple options for obtaining an MCA. It can be obtained with bad credit, without bank statements, no credit check, and even in 24 hours. So, even if you don’t have a good credit score, you probably still have a chance to qualify for MCA funding one way or the other.

According to a report by Shopify, merchant cash advances have the highest approval rate of 87% in comparison to line of credit (79%) and business loans (70%).

3. Cost of borrowing

Lines of credit generally have affordable interest rates. But factors like credit history and collateral requirement are involved in deciding the exact interest rate, so it varies with each business.

Merchant cash advances use factor rates to determine the total repayment value, which can get expensive overall.

4. Funding speed

MCA can typically provide you with funds within 24-72 hours (some companies provide same-day-funding), whereas a line of credit may take longer to get approved, depending on your creditworthiness. If you need fast funding, MCA should be your go-to option.

5. Flexibility for businesses

A line of credit gives you the flexibility in how you use and repay the funds. Once you can repay, you can borrow again without reapplying all over again. So the credit limit gets full again, ready to be used.

An MCA works differently. The contract is one-time, meaning you get a lump sum and start repaying immediately from your sales, with no flexibility to borrow more with the same agreement.

Pros and cons of a line of credit

In this section, we will compare the pros and cons of a line of credit and a merchant cash advance one by one. It will help locate the areas of strength and weakness of each financing solution, so you can make an informed decision when choosing the right option for your business.

Pros of a line of credit

- Flexibility: With a line of credit funding option, you get access to a sum of money called a maximum limit, from which you can borrow and spend as much or as little money as you need. For example, if your credit limit is £10,000 but you only use £4,760, you’ll only be charged interest on that £4,760.

- Lower interest rates: A line of credit comes with lower interest rates (typically in the range of 4% -14%) as compared to other funding options, so it remains accessible to businesses with a tight budget, too.

- Build business credit: Just like a traditional bank loan, a line of credit can also help build your business’s credit history. When a business takes out a line of credit, it shows as a type of loan on its records. Responsible and timely payments indicate good financial management and improve the creditworthiness of a business.

Cons of a line of credit

- Difficulty to qualify: The eligibility requirement for a line of credit requires having a comprehensive credit history, which makes it difficult for new businesses to qualify for funding.

- Potential for overborrowing: A line of credit allows businesses to borrow funds repeatedly, with offers flexibility on one hand, a risk of irresponsible financial management on the other. If a business consistently depends on a line of credit to manage its finances, it indicates an underlying cash management problem, which can snowball into bigger problems in the future.

Pros and cons of merchant cash advance

Now, let’s explain the pros and cons of a merchant cash advance in detail.

Pros of merchant cash advance

- Quick access to cash: Most MCAs are approved within 1-3 days after submitting the application, which makes it a great option if you need cash fast.

- Easy approval process: Obtaining an MCA is easy. Unlike a line of credit, MCAs don’t rely heavily on your credit score. The only deciding factor is your business’s daily sales, specifically through card transactions. So, even if your credit score isn’t the best, but you have a significant track record of making card sales, you likely qualify for an MCA.

- No collateral required: Traditional loans require you to provide collateral, like equipment or property, for security against the funds. But with an MCA, you’re simply repaying through a percentage of your sales without the need for collateral. The risk associated with your business is calculated by assessing your past record of sales only.

- No spending restrictions: There is no restriction for businesses as to where to spend the MCA funds. The business can use them for any reason, like paying wages, buying new inventory, launching a new product, etc.

- Flexible repayments: The major plus of an MCA is the flexibility offered to businesses to make repayments according to their card sales volume, with no fixed minimum requirement. So, if sales are high, you can pay more. When sales are slow, you can pay less.

Cons of merchant cash advance

- Higher cost: Merchant cash advances typically have higher costs as compared to other financing options like bank loans or a line of credit. The factor rate of an MCA can equate to an annual percentage rate (APR) of 40% to 90% if we compare it to the interest rate of a bank loan.

- Dent on revenue: Daily or weekly MCA repayments reduce the total revenue of the business. Especially in slower months, when sales are already low, the constant repayment deductions become a burden for businesses.

Line of credit vs merchant cash advance: Which is better for your business?

When it comes down to the ultimate question: line of credit vs merchant cash advance, the ultimate choice depends on multiple factors that we have discussed below:

1. What’s your cash flow situation?

Is your business seasonal or does it generate consistent, year-round revenue? If your cash flow fluctuates, you may need the flexibility offered by a line of credit. It gives you the freedom to draw funds when needed and repay when the timing’s right.

2. How quickly do you need funds?

If time is important, then an MCA is the way to go. With funds available within 24-72 hours, they are a lifesaver when you’re facing urgent situations.

3. How’s your credit?

The condition of your credit score is the most critical factor in the line of credit vs MCA debate. LOCs typically require a business to have a good credit score, so if you meet the criteria, then an LOC is your best bet. Otherwise, choose the merchant cash advance option.

4. Cost considerations.

Let’s face it, no one wants to throw money down the drain. If keeping costs low is your top priority, an LOC usually wins. The lower interest rates make it a more affordable option, especially when you plan to repay the loan over an extended period.

5. How long do you need the funds?

If you’re planning for long-term growth or need capital for ongoing expenses, an LOC provides the kind of revolving credit that’s ideal for long-term use. You can borrow, repay and borrow again without reapplying.

6. What’s your risk appetite?

Do you like to play it safe, or are you comfortable with a little more financial risk? A line of credit offers more predictability, with set interest rates and clear repayment terms. An MCA is less predictable – while repayments fluctuate with your sales, the higher cost and impact on cash flow during slow periods make it riskier.

Want to be linked with reliable MCA providers in the UK? ComparedBusiness UK can help

If you’ve decided to opt for an MCA, ComparedBusiness UK can ease the process for you. We help you secure merchant cash advance funding from the top lenders in the UK. Just submit your requirements in less than 2 minutes and we will match you with the financial institutions in the UK. You can pick and choose the best option as per your business requirements.

FAQs

MCAs don’t impact your credit score because they don’t involve credit checks or report to credit bureaus. However, failure to meet repayment terms could lead to legal action, which may indirectly affect your credit.

Yes, you can use both a line of credit and a Merchant Cash Advance simultaneously, as long as you can manage the repayment terms of both. However, be cautious, as taking on multiple forms of debt can strain your cash flow and increase financial risk.

Yes, an MCA is a good option for businesses with bad credit, as approval is based on daily or weekly sales rather than credit history. MCA providers focus more on cash flow and sales volume, making it easier for businesses with poor credit scores to secure fast funding.