Merchant cash advance has become a popular financing solution for businesses facing cash flow challenges because it allows them to secure instant funding against a portion of their future card sales. MCAs are especially attractive for small businesses, salons, and restaurants because they do not appear as traditional debt in their accounting records.

But problems can arise when a business takes out multiple MCAs at the same time. The daily or weekly repayments from each MCA can add up over time, disrupting the cash flow of a business. MCAs also typically come with a high factor rate as compared to traditional lending options. When multiple MCA lenders are automatically deducting repayments from card sales, the total repayment can end up outweighing the financial benefit of the advances themselves. To resolve this, businesses can consolidate all their MCAs into a single debt.

In this blog, we will explore what merchant cash advance consolidation is and how it works, discuss a real-life example, and explain its types, advantages, and disadvantages.

What is Merchant Cash Advance Consolidation?

Merchant cash advance consolidation is a financial strategy that allows businesses to manage multiple MCAs by combining them into a single, more manageable payment plan. As businesses grow, they might take on several MCAs for cash flow needs or repay an existing MCA. This leads to overwhelming daily or weekly payments.

MCA loan consolidation combines these advances into one loan, typically with better terms, which results in the businesses gaining financial stability.

According to Adroil Market Research, the Merchant Cash Advance market is expected to grow at an annualised growth rate of 5.03% till 2029.

MCA debt consolidation example

A retail business in the UK has taken out three merchant cash advances totalling £90,000, with combined daily payments of £1000. This means it was repaying around £30,000 each month. Having such a large amount deducted monthly put a serious strain on the business’s profit and cash flow.

To resolve this, the business applies for MCA consolidation. The consolidation lender directly settles the three MCAs with the previous providers and offers a new repayment plan with revised terms and a longer contract. Now, instead of paying £1,000 daily to multiple lenders, the business makes a single monthly payment of £4,000 to the consolidation lender to settle the £100,000 loan.

Do you need a Merchant Cash Advance?

How does merchant cash advance consolidation work?

MCA consolidation works by securing a new loan, often from a specialised consolidation lender, to pay off multiple existing MCAs. Instead of juggling various high-interest payments, the business now has just one loan to manage.

The lender negotiates with the MCA providers on behalf of the business to reduce the overall burden of debt. This new loan usually comes with a lower interest rate and favourable terms.

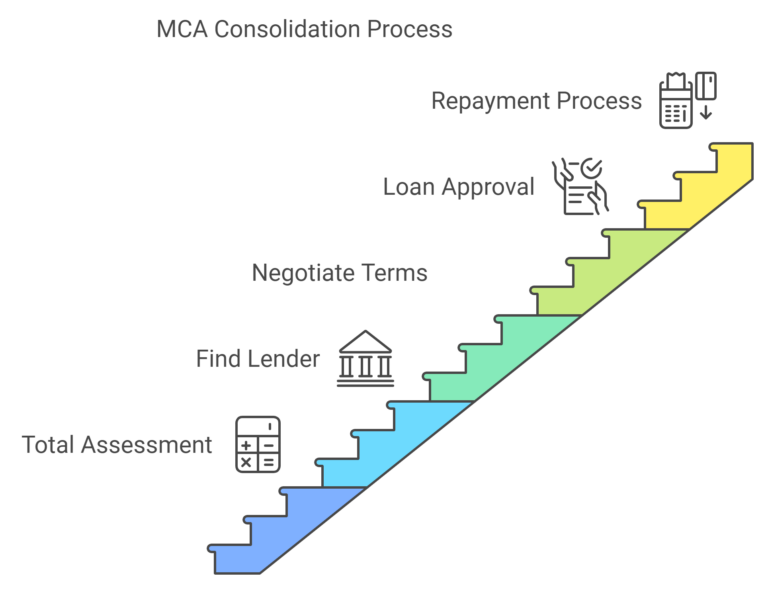

Process of MCA consolidation

The process of MCA debt consolidation involves the following steps:

- Analysing the total amount owed: The first step for a business is to assess the total debt from all merchant cash advances, including payment schedules, factor rates and the remaining balances from each MCA.

- Finding a lender: The business finds a lender who specialises in MCA consolidation. Before starting any negotiation, the lender will first evaluate the financial position of the business to determine its eligibility. The evaluation typically includes the same factors mentioned earlier. At this point, it’s helpful for the business to already have an understanding of its situation so it knows where it stands.

- Negotiating terms: Now, the consolidation lender negotiates with the old MCA providers to settle the debt. Depending on the type of MCA consolidation, the aim of this negotiation could be to extend the payment terms or reduce the overall repayment amount.

- Loan approval: Once this settlement is successful, the lender pays off the MCAs. The business now repays one loan to a single lender instead of keeping track of multiple monthly repayments of different MCAs.

- Repayment process: The business now begins repaying the consolidation loan according to the agreed terms.

3 types of merchant cash advance consolidation

| Option | Key Points |

|---|---|

|

Traditional MCA Consolidation |

|

|

Reverse Consolidation Loan |

|

|

Debt Settlement Program |

|

|

Credit Line Consolidation |

|

MCA consolidation can be approached in several ways, each with its benefits. Apart from the traditional MCA consolidation, there are three other methods.

1. Reverse consolidation loan:

A reverse consolidation lender does not pay off the existing MCAs. Instead, it makes the daily or monthly payments to the MCA providers on behalf of the business. In return, the business pays a new, lower daily amount to the reverse consolidation lender.

In this case, a business receives temporary relief from the heavy repayment burden of multiple MCAs by not repaying them themselves. However, it is still responsible for repaying the full advance amount and factor rate of each original MCA, plus an additional fee charged by the reverse consolidation lender.

2. Debt settlement programme:

In a debt settlement programme, a third-party company directly negotiates with MCA providers to reduce the total amount a business owes. This option is typically considered a last resort for businesses that are struggling to keep up with the repayments or are at risk of default. Once the programme begins, the business stops making the repayments to the lenders. Instead, the repayments get accumulated in an account managed by the settlement company. When enough funds are collected (usually 50-70% of the total debt), that’s when the negotiation process starts.

If an MCA lender and the company come to a mutual agreement, the funds are used to pay off the debt, one MCA at a time. Special emphasis on the ‘if’ because the lenders are not obliged to accept the settlement offers. In exchange for the service, the settlement company charges 15% – 20% of the saved amount to the business.

Even though this programme allows a business to settle its debts by paying a portion of its original debt, it can damage the business’s credit score and harm its future financial credibility.

3. Credit line consolidation:

Credit line consolidation involves using an existing or newly established business line of credit to pay off multiple merchant cash advances. A business line of credit gives the business access to an account with a set limit of funds, from which it can withdraw as needed. The interest is charged only on the amount used, while the rest of the funds stay available until the limit resets.

Similarly, a business uses a line of credit to pay off all its MCAs. After that, it repays the loan on flexible terms to a single line of credit lender.

Pros & cons of merchant cash advance consolidation

| Pros | Cons |

|---|---|

|

Simplifies repayment with a single monthly payment. |

Long-term costs can rise due to extended repayment periods. |

|

Improves cash flow by reducing monthly payments. |

Fees can be expensive, including hidden costs. |

|

Helps avoid default by restructuring debt. |

|

|

Offers customised repayment plans for flexibility. |

|

Weighing the advantages and disadvantages of MCA consolidation is important. How else will you be able to arrive at a decision?

Pros of MCA consolidation

- Simplifies repayment process: One big benefit of MCA consolidation is the flexible repayment structure. Consolidation takes it one step further. It does this by combining multiple advances into a single monthly payment. With one predictable payment, it’s easier for your business to budget.

- Improves cash flow: Consolidation can reduce the total amount you need to pay each month, freeing up cash flow for other business expenses. This way, you may allocate more funds to growth activities.

- Avoids default: If your business is at risk of defaulting on one or more MCAs, consolidation can help prevent this by reconstructing your debt into more manageable terms.

- Customised repayment plans: Many MCA consolidation providers offer customised repayment plans that are directed towards your business’s needs, hence providing flexibility standard MCA agreements often lack.

Cons of MCA consolidation

- Long-term costs can rise: While MCA loan consolidation might lower your monthly payments, it can also extend the repayment period. This could result in higher overall interest costs over time.

- Fees can be expensive: Some consolidation programmes come with upfront costs, including origination fees and service charges. Be cautious of hidden fees that could make your consolidation less cost-effective.

What to consider before choosing merchant cash advance consolidation?

When considering an MCA consolidation loan, it’s important to consider the following factors to make sure you have chosen the right solution that aligns with your business needs:

- Current financial condition: Evaluate your monthly profit, expenses, cash flow, and total MCA repayments.

- Total debt load: Calculate the total amount of debt your business is carrying from all Merchant Cash Advances. This helps in determining the right consolidation approach, whether it’s a reverse consolidation loan or another type of consolidation.

- Costs and fees: Each MCA consolidation method comes with its own cost, including interest rates and possible penalties. Compare these costs against your current MCA obligations to find out if consolidation will save money in the long run.

- Repayment terms: Consider the length of the repayment period associated with the consolidation option. You’re trying to pay an existing debt, not tying up your feet with another cruel one.

- Reputation of the consolidation provider: Ensure that the consolidation lender has a solid reputation. Check reviews, ask for references and verify their experience in dealing with MCA consolidations.

Explore top merchant cash advance options in the UK with ComparedBusiness UK

ComparedBusiness UK can help you secure merchant cash advance from the top vendors in the UK. Just submit your requirements in less than 2 minutes, and we will match you with the top financial institutions in the UK. You can select the most suitable option based on your business needs.

FAQs

MCA consolidation involves combining multiple cash advances into a single loan with more favourable terms. This simplifies repayments, often lowering the monthly amount and helping businesses manage their cash flow more effectively by reducing high MCA fees and interest rates.

MCA consolidation can enhance cash flow, reduce total interest rates, and streamline repayment plans into one monthly payment. This is especially beneficial for companies managing several MCA payments, which can be burdensome and expensive.

MCA consolidation may stretch the repayment duration, thereby possibly raising the total interest paid over time even when it can lower monthly payments. Consolidation can also include costs, and some MCA lenders could enforce prepayment penalties.