Single invoice factoring (also known as spot factoring) can be simply explained as invoice factoring without its long-term contracts. If a business is facing financial challenges but doesn’t want to factor all its invoices, single invoice factoring offers the perfect solution for it. With this approach, there is no requirement for a business to sell every invoice; instead, it can choose to factor one or more of its high-value invoices as needed.

Let us now explore how single invoice factoring works in detail so you can decide whether it is suitable for your business.

What is single invoice factoring?

Unlike traditional invoice factoring, where you sell off all your outstanding invoices, single invoice factoring lets you pick and choose which invoices to factor. Think of it as a pay-as-you-go financing option. You sell one unpaid invoice to a factoring company in exchange for an immediate cash advance. Once your customer pays, you get the rest, minus fees.

Cost of a single invoice factoring

Generally, the costs of single invoice factoring = the cost of accounts receivable factoring. The most significant cost is the factoring fee, which ranges from 1% to 5% of the invoice value. For example, an invoice worth £10,000 might incur a 3% fee, meaning you’d pay £300 for the service.

Now, some factoring companies may charge additional fees, such as administrative costs or late payment fees, depending on how long it takes your client to pay. But this is not common. However, it is crucial to read the fine print while making the agreement and asking for a full breakdown of costs.

Compare Invoice Financing Quotes Today

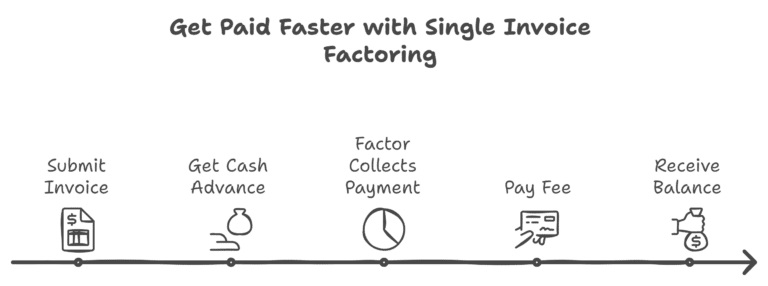

How does single invoice factoring work?

1. The business submits an invoice

The business initiates the single invoice factoring process by submitting the specific invoice it wants to factor. This invoice must be fully completed; that is, the products or services mentioned must have already been delivered to the customer for it to qualify for evaluation.

2. The factoring company assesses associated risk

Qualification standards vary with each provider in the UK, but one thing that remains constant is the creditworthiness of the business’s original client. The factoring company calculates the risk associated with an invoice concerning the client’s payment history. Depending on whether the agreement is for recourse or non-recourse factoring, the factoring company also assesses the risk of non-payment. Typically, fresh invoices with short payment terms (20-30 days invoice issued a week ago), are considered less risky compared to older invoices with lengthy payment terms (90 days invoice issued 2 months ago).

All these factors take part in determining whether the factoring fees will be towards the higher end or the lower end. This whole process takes about 1-2 days, generally.

3. The business receives a cash advance

Once the evaluation is completed, the factoring company will provide you with the cash advance, which ranges from 70% to 90% of the total invoice value. The exact amount of funds for a business depends on different factors like:

- The specific business industry.

- The length and value of the invoice.

- The creditworthiness of the business’s client.

- Whether the single invoice factoring type is recourse or non-recourse.

4. The client pays the invoice

In single invoice factoring, the business sells its unpaid invoices to the factoring company, also transferring ownership of the invoice in the process. The factoring company then manages the whole payment collection process.

5. The business pays the factoring fee

When the client fulfils the payment term and fully settles the invoice, the factoring company sends the remaining 10% to 30% balance to the business, minus the factoring fees.

Why do businesses opt for single invoice factoring?

Let us discuss the three key reasons why businesses opt for single invoice factoring:

- To access funds: The main reason businesses choose to sell their invoices is to gain instant funds and improve their cash flow.

- Flexibility to select an invoice: Single invoice factoring gives them the freedom to choose the invoices to factor, which makes it an attractive option for small to medium-sized businesses.

- Short-term contract: The short-term nature of the single invoice factoring contracts makes it feasible for businesses to opt out as needed. This is particularly useful for businesses with seasonal peaks or irregular cash flows.

Advantages and disadvantages of single invoice factoring

| Advantages | Disadvantages |

|---|---|

|

Offers flexibility to choose a specific invoice to factor. |

Ownership of the invoice transfers to the factoring company. |

|

Provides fast access to cash. |

Risk of over-dependence on external cash support. |

|

Doesn’t show as debt on accounting records. |

Limited available services. |

|

Usually have short-term contracts. |

|

Benefits of single invoice factoring

The following are the advantages of single invoice factoring for small businesses in the UK.

1. Flexibility to choose invoices to factor

With single invoice factoring, a business can factor invoices entirely on its terms. There is no requirement to meet a minimum limit, as businesses can choose to factor as few as one invoice. Typically, businesses use single invoice factoring to sell a few of their high-value invoices to a factoring company. The rest of the invoices continue as usual and with no effect on those clients.

2. No long-term contracts

Single invoice factoring contracts are typically short-term as compared to standard invoice factoring agreements because of the smaller number of invoices involved. Once the selected invoice in the agreement gets paid, no matter how much time it takes, the business receives the remaining balance, pays the factoring fee, and the contract comes to an end.

3. Instant access to cash

A business can typically access funds within 24-48 hours after the factoring company completes the evaluation process of the submitted invoice and the related client. There is no restriction as to how these funds must be spent. A business can use the cash advance to clear any of its expenses, like upgrading its space, launching a marketing scheme, building a new product or clearing the payroll of its employees.

4. Not a debt for a business

One of the reasons why business owners choose factoring is that it differs from traditional loans. Unlike bank loans, single invoice factoring doesn’t appear as debt on a business’s balance sheet. That is because it doesn’t involve borrowing money or repaying it on an interest basis; instead, it simply means selling an asset, which is your invoice.

5. Strengthens client relationships

The factoring company is responsible for taking payments from your customers, which can sometimes become confusing and untrustworthy for them. This is one of the biggest disadvantages of factoring. But with single invoice factoring, you can choose to only sell selective invoices, which means the rest of your clients remain unaffected.

You keep collecting payments from them yourself.

Downsides of single invoice factoring

While selective invoice factoring can be a great way to ease cash flow issues, it’s not without its risks.

1. Impact on client relationships

Once you sell your invoice to the factoring company, they take over the collection process. While most reputable factoring companies in the UK are professional, some clients may not appreciate dealing with a third party. If the factoring company handles collections poorly, it could harm your reputation or even damage your relationship with your client.

2. Cash flow dependency

Relying on single invoice factoring for quick cash might solve today’s problem, but it could create a bigger issue down the road. If your business becomes too dependent on factoring to keep the cash flowing, you may find yourself stuck in a cycle where you’re continually selling invoices to cover immediate expenses.

3. Limited companies available

Some cities in the UK might not have factoring companies that offer selective invoice finance facilities. This can create serious issues as you’re left without any options. But don’t worry, with ComparedBusiness UK, you will be linked with top lenders who provide single invoice factoring services to you.

Is single invoice factoring right for your business?

Well, like most things in business, it depends on your situation. If you’re facing a short-term cash crunch and don’t want to lock yourself into a long-term contract, selective invoice factoring could be a breath of fresh air.

However, it’s essential to remember that factoring isn’t a free ride. The costs, while manageable for one or two invoices, can add up if you make a habit of it. And let’s not forget the potential for client friction if the factoring company doesn’t handle collections as smoothly as you’d like.

In short, single invoice factoring works best when used strategically.

Get In Contact With Top Single Invoice Factoring Lenders With ComparedBusiness UK

Securing a single invoice factoring deal for your business is easy with ComparedBusiness UK. We provide you with secure invoice factoring quotes from top providers in the UK. Just submit your requirements in less than 2 minutes, and we will match you with them. Time to solve your cash flow problems today.

FAQs

Single invoice factoring gives businesses the flexibility to sell one specific invoice for cash, rather than factoring all of their invoices through long-term contracts. This financing option is ideal for businesses needing occasional funding without being drawn into long contracts.

Funds through single invoice factoring or spot factoring can be accessed within 24-72 hours after submitting an invoice. This fast process makes it a great option for businesses stuck with financial emergencies.

Factoring fees typically range between 1% to 5% of the invoice value, and the advance rate is usually 70%-90%. While it could be more expensive than traditional loans, it provides faster access to cash, which can outweigh the costs for businesses facing urgent financial needs.