Accepting card transactions in addition to cash payments can broaden the customer base of a business and bring in more sales in the long run. But, at the same time, these card transactions (credit and debit) also incur a cost for your business. In this blog, we will first understand the different costs involved in carrying out a credit card transaction. After that, we will discuss 6 strategies for businesses to process credit card transactions while also saving money efficiently.

What is a credit card transaction?

A credit card transaction works differently from swiping your debit card to pay for a product or service. In a credit card transaction, the bank carries out the transaction with the funds lent to the cardholder. The cardholder must pay them back within a certain time with an interest rate specified by the bank.

The repayment process is between the customer and the bank, and the merchant (a business that received the funds) is not involved at this stage. However, since the business initiates the transaction and receives the money, it is concerned with covering the processing fee of a credit card transaction. That is why it is important to learn how it works to better understand the process.

What is a card machine?

A card machine or a PDQ machine allows businesses to process card-based transactions, whether they are credit or debit. In this way, they can offer multiple payment options to their customers, in addition to dealing in cash. Today, we are more concerned with how card machines help businesses process credit card transactions, so we’ll focus more on this aspect.

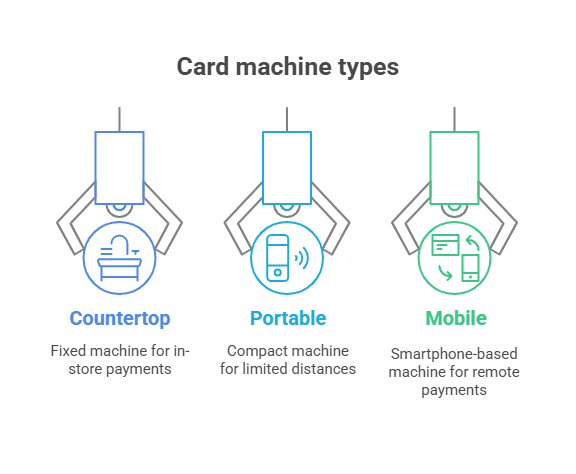

Types of card machines

It is important to know the different types of card machines available in the market because each caters to a unique set of business needs. Choosing the right card machine for your business will allow you to maximise its benefits and use it efficiently to justify its associated costs. A business also needs to decide between buying a card machine or renting one. We have discussed this topic in detail later in the blog, so let us go over the 3 types of card machines for starters.

- Countertop card machine: This type of card machine is fixed at a place in a physical store. It is connected to the main POS system via wires, so payments are processed exactly where they are made.

- Portable card machine: It is a compact card machine that can be used remotely inside a specific premise of up to 100 meters.

- Mobile card machine: With the help of a card reader, a smartphone with internet connectivity can be converted into a mobile card machine. It can be operated flexibly over large distances as long as it has an internet connection.

6 Cost-effective strategies: At a Glance

| Strategy | Key Point |

|---|---|

|

Choose the right card machine. |

Avoid paying for features you don’t need. |

|

Buy instead of rent if possible. |

Buying saves more long term if you process lots of transactions. |

|

Pick the right pricing structure. |

Understand pricing models before committing to a provider. |

|

Accept only cost-effective cards. |

Decline cards with high processing fees to protect profit margins. |

|

Favor in-person over online. |

Physical payments are more secure and cheaper to process. |

|

Negotiate and compare providers. |

Ask for lower processor fees and compare offers before signing a contract. |

6 ways to process credit card transactions while saving money

There are many practical steps you can take to reduce the credit card transaction-related costs. Let’s start with the simple ones and then work our way to the rest.

1. Choosing the right card machine

The card machine you choose to buy will play an essential part in shaping your credit card transaction fees in the long term. You could end up with extra features, a monthly fee, and a minimum transaction limit that your business doesn’t even need if you choose the wrong card machine. We have already talked about the 3 different types of card machines earlier, so now we will get into the details of whether you should buy or rent your preferred card machine.

Should you rent or buy your card machine?

When you rent a card machine, providers offer a minimum 6 to 12-month contract that can even go up to years. These providers offer lower transaction rates for a longer commitment, which might look like you are saving money at first, but in reality, the monthly rental costs build up over time. In the end, it becomes difficult to end the contract early because of the cancellation fees and other additional terms.

Now, buying the card machine is the other option. You have to pay for the machine upfront, which could be a financial burden for small-scale businesses. But if your business processes a considerable amount of credit card transactions, buying the machine can save you money by saving you from monthly rental payments.

| Option | Cost Range | Paying option |

|---|---|---|

|

Buy a card machine |

£19-£230 + VAT |

One-off upfront fee |

|

Rent a card machine |

£10-£30/month |

Regular monthly costs |

2. Be selective about the cards you accept

With every transaction your business processes, a percentage of it gets deducted for carrying out the process. It is often called a transaction fee, processing fee, or merchant service charge. On average, it is calculated at 1.5%-3.5% of each transaction. It includes three different costs that arise during the transaction and have different destinations.

- The interchange fee goes to the customer’s bank for authorising the transaction and transferring the funds.

- The scheme fee goes to the card network, like Visa or Mastercard.

- Processor markup goes to the payment provider used by the business.

The percentage of the scheme fee can vary greatly with the type of card network your customers use. With premium cards, customers get benefits (discounts, lower interest rates, flexible payment windows, etc.), so such transactions prove expensive on the business end because they have a higher processing fee.

Your business can refuse to accept cards with a higher processing fee and offer cash payment alternatives for such customers. Of course, this means your customers will have fewer options to choose from, but being selective can protect your business’s profit margins in the long run.

3. Select a suitable pricing structure

Before choosing a card machine provider, make sure you understand how the pricing works with most of the card processors in the market. Let us look at the 4 main types of pricing that are most common.

- Subscription-type pricing: People tend to confuse it with the flat rate pricing structure, but both are different. Your provider charges you a flat monthly fee and carries out transactions for the rest of the month.

- Tiered Pricing: In this pricing strategy, your card provider divides all your credit card transactions into different categories, like qualified, mid-qualified, and non-qualified, with different processing costs criteria for each category. The catch is that the provider does not disclose the requirement to each category, so it is almost impossible to predict how much your business will have to pay.

- Flat rate: Flat rate means your card provider will charge you the same cost for every credit card transaction, independent of the volume of transactions or the type of card.

- Interchange plus pricing: It clearly tells us about the percentage of the total processing fee that goes towards the customer’s bank and what is kept by the provider as profit. This is preferred by most businesses because it is easy to understand and also offers transparency.

4. Fulfil a long-term contract with your provider

If you have done your research and are confident in what you know, consider committing long-term with your card payment provider. This will get you noticeable perks like lower transaction fees per sale, free setup (when you buy a card machine), regular maintenance of the machine, and much more. These savings can quickly catch up in no time.

5. Physical vs online credit card transactions

Online transactions are the most convenient for customers. But they prove to be expensive for businesses as compared to in-person transactions. The reason for this difference has to do with the risk associated with both types of transactions.

- Physical transactions tend to be more secure as they are processed at the same moment the cardholder enters their details into the card machine. In case of a fraudulent transaction, the transaction gets declined on the spot.

- Online transactions are more risky for the banks because the cardholder is not physically present. There is no way to verify the person behind the screen. With online credit card transactions, additional security measures like payment gateways, customer protection, and encryption tools are also employed, which contribute to the total cost too.

6. Negotiate lower rates and shop around

If your business handles a high volume of transactions each month, you are in a position where you can negotiate flexible terms with your payment processor. It is best to discuss this before reaching a contract with your provider. Don’t be discouraged if one of the providers doesn’t agree to your terms, because that brings us to discuss our next point, which is the importance of comparing different providers and their pricing rates.

Even though you can’t negotiate on the fixed pricing of the banks and card networks, the markup margin (profit gained by the processor) can be discussed. Don’t be afraid to ask questions because a small reduction in fees can add up to big savings over time.

Compare trusted providers with ComparedBusiness UK

If you’re planning to negotiate better rates or simply want to look around, why not start with the best in the business? We at ComparedBusiness are experts in linking you with top card payment processing solutions. Just submit your business details in less than 2 minutes, and we will get back to you with quotes from the list of top card machine providers in the UK.