Following up with clients and chasing payments after delivering a service and an invoice requires consistent administrative effort. It requires people, resources and time to collect the unpaid payments successfully. If the process is not managed efficiently, it can lead to late payments from customers, which ultimately disrupts the cash flow and affects business operations.

What is collection factoring?

In collection factoring (also called maturity factoring), a business sells its unpaid invoices to a factoring company with the main goal of transferring the responsibility for payment collection to a third party. The business continues its work as usual, while the factoring company handles payment collection on its behalf from the customers.

According to a report by Invoice Funding UK, the factoring market size was estimated at £3 billion in 2024.

4 collection factoring concepts you need to know

You need to understand the following 4 concepts involved in the collection factoring process:

- Business: The company that initiates the collection factoring agreement by selling its unpaid invoices to a factoring company.

- Customers: The clients responsible for paying the invoices.

- Factoring company: The third-party company that collects the invoice payments from the customers on behalf of the business.

- Collection fee: The fee charged by the factoring company to carry out the payment collection process.

Compare Invoice Financing Quotes Today

How collection factoring works in 3 steps

1. Initiating the collection factoring process

The process starts when a business assigns its unpaid invoices to a factoring company. These invoices show the money owed to the business against the services or products provided to the customers.

2. Collecting payments from end clients

After establishing the collection factoring agreement, the factoring company interacts with the customers, keeps track of the payments, gives payment reminders to the customers consistently and looks after the collection process in place of the business. A good factoring company prioritises professionalism to protect your customer relationships.

Read our article on silent factoring if you’re highly concerned about your customer relationships being weakened with a third-party collection system.

3. Transferring the collected funds to the business

After all the customers have cleared their invoices, the factoring company passes the total funds minus the collection fee to the business.

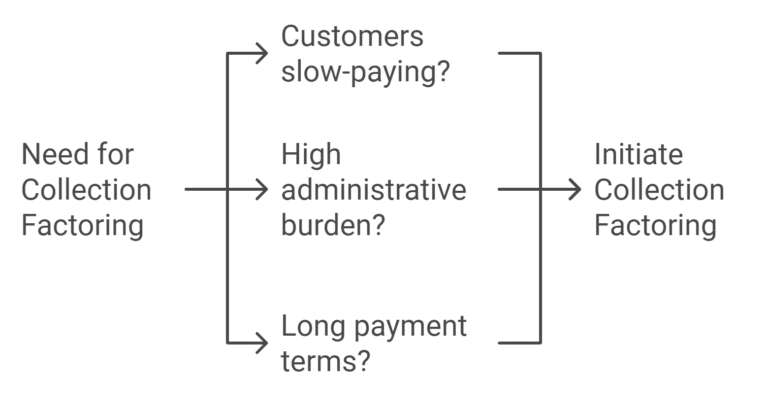

When should a business consider collection factoring?

If your business shows at least two of the following signs, collection factoring could be a smart solution:

1. Slow-paying customers

Having slow-paying customers can depend on several factors, like your business industry, whether you deal in products or services, and the average payment cycles. Regardless of the cause, waiting for payments can drain your attention, which could be better spent on other tasks. With collection factoring, the factoring company oversees following up on payments. When a third party exclusively focuses on collecting payments from customers, there is a higher chance of getting paid on time.

2. High administrative workload

Handling the payment collection process can be time-consuming. If your team is spending too much time and money chasing unpaid invoices, outsourcing this task to a factoring company could be a better alternative. This relieves you from the stress of chasing invoices and frees up your staff so they can focus on core business activities.

3. Long payment cycles

One of the major reasons why businesses opt for factoring is when they operate in industries where standard payment cycles are calculated in months rather than days. It is common in sectors like construction, architecture or research services, where businesses deal with extended payment timelines. With the payment terms already long, late payments can harm the cash flow. Collection factoring helps ensure payments are received promptly to keep the cash flow cycle predictable.

According to a report by Invoice Funding UK, payment cycles of businesses have been around 45 days in 2022.

Pros and cons of collection factoring

Let us discuss some benefits that businesses receive via collection factoring. Like any other invoice financing option, we also have to consider the cons alongside the pros.

Pros of collection factoring

- Steady cash flow: When a factoring company is dedicated to collecting payments, it sends reminders to customers and regularly follows up with them. Clients tend to pay timely with a due collection process set in place. It largely contributes to keeping the cash flow steady.

- Less workload: By assigning a factoring company to collect payments in your place, you save valuable time and resources in exchange for a small collection fee.

- Secure customer relationships: A good factoring company acknowledges the importance of maintaining customer relationships. They deal with the customers professionally, so you don’t risk your reputation by repeatedly chasing them for payments.

- No need for a high credit score: Collection factoring focuses more on the financial reliability of your customers than your business’s credit history. Even if your business doesn’t have a high credit score, you can still access a collection service, unlike traditional lending options.

Cons of collection factoring

- No upfront cash: Collection factoring doesn’t offer immediate cash advances. If your primary need is fast liquidity, this might not be the best solution. Instead, it’s better suited for businesses that want help managing collections.

- Fees and costs: Collection factoring isn’t free. Factors charge service fees, which may eat into your profit margins. If you’re working with skim margins, the cost of factoring might outweigh the benefits.

| Pros | Cons |

|---|---|

|

Ensures timely collections, leading to more predictable cash flow. |

Doesn’t offer immediate liquidity like invoice factoring. |

|

Outsourcing collections saves time and internal resources.

|

Service fees may reduce profit margins, especially for small businesses. |

|

Professional collection prevents strain on customer relationships. |

|

|

Focuses on customer creditworthiness, not the business's credit. |

|

Collection factoring vs invoice factoring

When comparing collection factoring to invoice factoring, the primary difference lies in how businesses use each financing solution to achieve different objectives.

- With invoice factoring, a business receives an upfront cash advance (about 70-90% of the invoice value) to cover any immediate expenses and restore the cash flow. It is mostly used by businesses facing cash flow issues caused by late payments from their customers.

- Collection factoring doesn’t offer immediate cash like invoice factoring does. So, the businesses that choose collection factoring don’t necessarily mean they are in any financial trouble. Instead, they use it as a tool to transfer the administrative workload of collecting the payments to a third company. With that, they aim to receive timely customer payments without the burden of chasing the invoices themselves.

- While the factoring company also collects payments from customers in invoice factoring, this usually occurs as a byproduct of the process rather than its primary purpose.

How to choose a collection factoring provider?

Choosing the right collection factoring provider can be a big help for your business. But how do you pick the right one when there are so many options?

- Reputation and experience: First things first – reputation matters. Is the provider established and experienced in your industry? A provider with a strong track record in handling businesses similar to yours can offer peace of mind. Reviews, referrals and testimonials can give you a clear picture of their reliability.

- Transparent fees and terms: The process comes with fees, and some providers can sneak in hidden charges. When comparing providers, be sure to get a full breakdown of their fees – service charges, collection fees and any hidden costs lurking in the contract.

- Quality of customer service: You’re not just looking for a vendor; you’re looking for a partner. That means the factoring provider should be responsive, communicative and transparent. Are they easy to reach when you have questions? Find that out.

- Funding speed: How quickly can the provider get you the cash once payments start coming in? Even though collection factoring doesn’t typically involve upfront advances, you’ll still want to ensure they remit payments promptly after invoices are settled.

Get Free Collection Factoring Quotes with ComparedBusiness UK

Getting reliable collection factoring services in the UK is easy with ComparedBusiness UK. Just submit your requirements in less than 2 minutes, and we will match you top collection factoring service providers in the UK.

FAQs

Collection factoring outsources the collection of overdue invoices with no upfront cash advance, whereas invoice factoring offers an immediate advance depending on the invoice value. It is suitable for organisations that need assistance with collections but do not require immediate cash.

Collection factoring works well for businesses with long payment terms, seasonal cash flow gaps, or customers who take their time settling invoices. It’s especially handy for industries like manufacturing, logistics, or professional services, where chasing down unpaid invoices can eat up time that could be better spent elsewhere.

Unlike traditional loans, collection factoring focuses more on your client’s ability to pay rather than your business’s credit score. So, even if your company has less-than-ideal credit, you could still qualify if your clients have a strong history of paying their invoices on time.