What is debt factoring?

Being in a debt factoring agreement means that a business has sold its unpaid invoices to a third party in return for quick cash assistance. This need for extra cash flow could be due to many reasons, like delayed payments from customers, having to wait on long-term invoices, slow business season, or unexpected business expenses.

With this invoice factoring technique, a business receives 70% – 90% of the total transaction value of its unpaid invoices at the start of the agreement. Meanwhile, the third party (also called a factoring company or simply a factor) collects the pending payments from the customers. Once all the original invoices are cleared, the factoring company then transfers the remaining 10% – 30% of the invoice value minus the factoring fee to the business.

According to IBIS World Report, the revenue of the factoring industry in the UK has grown at a CAGR of 3.5% over the past 5 years.

Key Debt Factoring Terms

Let us go through the key terms involved in the debt factoring process. Later in the blog, we will see how they work together to carry out the actual service.

- Factoring company: It is a financial institution or third-party firm providing the debt factoring service and buying unpaid invoices from the business.

- Business: The entity availing the debt factoring service by selling its unpaid invoices to the factoring company.

- Debt factoring rate: The business pays this fee to the factoring company in return for receiving the debt factoring service. It is calculated as a percentage of the total value of the sold invoices. Typically, it ranges from 1% to 5%, depending on factors like the business industry, number of invoices, contract duration, the past financial track of a business, and more.

How does debt factoring work?

Remember the key terms we explained before? Let us see how each of them plays its role in the debt factoring process.

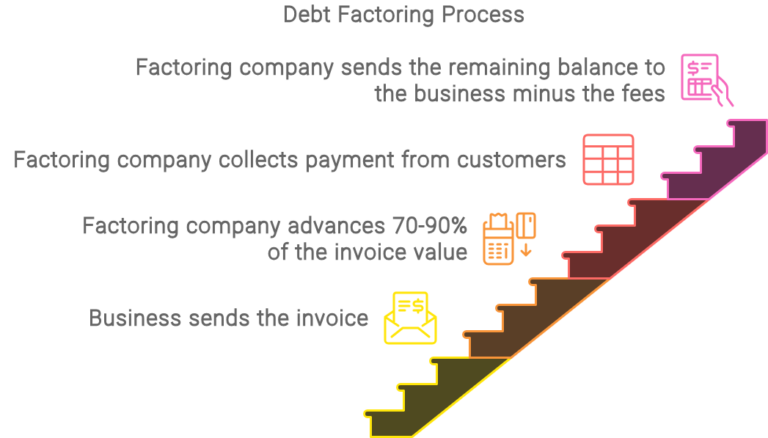

- Drafting the invoices: The business sells its product or service to its customers and generates the invoices, highlighting the type and number of products sold, business terms, the customer’s information, and the length of the invoice (typically ranging from 6 to 12 months or more).

- Handing the invoices over to the factoring company: Sometimes clients delay paying the invoices, or at other times, the payment period is too long. In such cases, waiting for months to receive payments can slow down business operations and negatively impact the cash flow. So, the business sells the unpaid invoices to a factoring company to receive 70% to 90% of the invoice value upfront.

- Collecting customers’ payment: The responsibility of collecting the full payments from the business’s clients transfers from the business to the factoring company. Once the total payment is collected, the business receives the remaining balance minus the factoring fee.

Real Life Debt Factoring Example

Let’s say a small manufacturing company has issued an invoice of £50,000 to a client, with payment due in 60 days. Then, the company decides to debt factor the invoice under the following conditions:

> 85% advance payment and 2% factoring fee.

Advance payment = 85% of £50,000 = £42,500

Money left with the factoring company = £7500

Factoring fee = 2% of £50,000 = £1000

Final amount paid to the business after the customers have paid = £7500 – £1000 = £6500 + £42,500 = £49,000

Compare Invoice Financing Quotes Today

Is Debt Factoring the Right Choice for Your Business?

Let us discuss 4 scenarios in which it would make perfect sense for any business to opt for debt factoring.

- To expand & grow: If a business wants to grow and scale its operations, it needs extra cash flow to support the additional expenses. In such a scenario, going for a debt factoring service is recommended. That being said, debt factoring is most effective when used to fund a short-term growth plan that gives returns relatively quickly.

- Lengthy invoice-payment periods: Businesses often extend the payment period for their invoices to accommodate their customers, provide flexibility, and promote good customer relationships. This creates a lack of capital or liquidity for a business and slows down its capability to scale, grow the team, invest in research or take on new projects. The extra financial assistance from debt factoring helps fill in this liquidity gap.

- Persistent cash flow problems: If a business is constantly forced to compromise its operations due to a lack of cash, it can snowball into bigger problems over time. These cash flow problems get easily solved with the help of an advance obtained through debt factoring.

- Avoiding bank debt: Debt factoring is not like a traditional loan or debt. It is simply selling something a business already owns (unpaid invoices). That is why businesses that want to avoid taking bank debt should opt for debt factoring.

Types of debt factoring

1. Recourse factoring

Process: In recourse factoring, the factoring company provides an advance rate to the business, just like in debt factoring. If the customer fails to pay the invoice, the business is responsible for providing a refund to the factoring company.

Benefits: Since the factoring company has less risk, fees are generally lower. Moreover, the business retains control over customer relationships and collections.

Drawback: If the customer fails to pay, the financial burden falls on the business.

2. Non-recourse factoring

Process: In non-recourse factoring, the factoring company takes the risk of non-payment. It buys the invoices and is responsible for collecting payments. If the customer fails to pay the invoice, it absorbs the financial damage.

Benefits: The business remains protected from the risk of non-payment.

Drawback: Higher fees because of the high risk borne by the factoring company. Also, the factoring company may impose strict credit checks on customers, which can limit the invoices that can be factored.

Read more about the difference between recourse and non-recourse factoring.

Advantages & disadvantages of Debt Factoring

| Advantages | Disadvantages |

|---|---|

|

|

Opting for debt factoring can be a tricky choice. But if you’re knowledgeable about its pros and cons, you can easily weigh its scope according to your business requirements.

Advantages of debt factoring

- Improved cash flow: How can debt factoring help cash flow? Well, debt factoring provides immediate cash to the business. This quick injection of funds can help them to cover their daily operations, pay suppliers, fulfil payroll and invest in time-sensitive opportunities.

- Frees up the responsibility of collection: When businesses engage in a debt factoring agreement, the responsibility of collecting payments from the customers falls onto the factoring company generally. This not only saves time but also allows businesses to focus on core activities.

- No debt incurred: Another advantage of factoring is that unlike traditional loans, debtor factoring is not a form of borrowing. It doesn’t add to your company’s liabilities. This means your balance sheet remains unaffected, and you don’t have to worry about a reduction in your credit score.

- Flexible financing options: Thanks to the different types of debt factoring, your business gets multiple financing options with variable terms. This means you can choose the conditions that suit you the most.

Disadvantages of debt factoring

- Costly fees: The first debt factoring drawback is its fees. These service fees can reduce your profit margins, making it difficult to run the business sustainably.

- Customer relationships can be damaged: Handing over invoice collection to a third party can sometimes lead to concerns among customers, particularly if the factoring company employs aggressive collection practices.

How to choose a Reliable factoring company?

The factoring market in the UK is huge, and it can become difficult to choose the right factoring company. To make it easier for you, we have compiled a list of criteria that you should consider to spot a reliable factoring company:

- Years of working in the industry: The experience of a factoring company denotes its reputation, experience, and customer satisfaction. If a factoring company has been in business for a long time, it is a green flag for its authenticity and reliability.

- Customer reviews: When comparing factoring companies to choose the best one, make sure to look at the reviews of their previous customers. This will help you understand their business values and how they treat their customers, and see if it aligns with your preferences.

- Advance rate: It is the sum of money (70% – 90% of the invoice value) provided upfront. After evaluating your business criteria, the factoring company will give you a specific quotation of the advance rate. See if it aligns with your requirements; if not, you can negotiate the percentage with the company or simply look for a different option.

- Terms and conditions of the agreement: Carefully read the terms of the debt factoring agreement, like the length of the contract, the percentage of advance rate, cancellation fee, service quality clauses, and any additional fees before closing the deal.

ComparedBusiness UK provides you with top options for debt factoring

We at ComparedBusiness UK are experts in saving your time and money. Just submit your requirements in less than 2 minutes, and we will get back to you with quotes from a list of top debt factoring providers. You can pick and choose the best option for your business.

FAQs

Debt factoring doesn’t have a traditional interest rate like a loan. Instead, factoring companies charge a fee, often between 1-5% of the invoice value. This depends on factors like the creditworthiness of your customers and the invoice amount.

Drawbacks of debt factoring involve high fees that can reduce profit margins and potential concerns about dealing with a third-party collector.

A factoring debtor is the customer of the business who owes payment on the invoice that has been sold to the factoring company. The factoring company collects the payment directly from this debtor, relieving the original business of the collection responsibility.